A Market Showing Genuine Promise

At Carlyle Kingswood Global, a leading international recruitment firm, we are pleased to report on the London private practice legal market as we e...

Connecting...

Law firms have become far more corporate. The laissez-faire approach that characterised many partnerships in the halcyon mid to late 1990s has, in many firms, given way to a more disciplined approach to both the business and the practice of law and perhaps, at last, to the realisation that separating the two represents a false dichotomy. Some firms have ceased to be, either through dissolution or through being merged into others.

As we stand now in 2015, things look quite promising for the UK legal profession. Half-year figures published by law firms at the end of 2014 have been generally positive and almost all of the larger law firms expect revenues to increase - nearly half of them expect increases of between 10 and 20 per cent.

Does this mean that sustained growth has returned to the legal sector? If so, how long is it likely to last? Has the legal sector reached its pre-recession peak yet? If not, when are we likely to see that? What is the likelihood of another economic recession that would slow growth or perhaps even reverse it? Is the increase in demand for legal services translating into increased profitability? What should law firms be doing in order to capitalise on the trend?

These are all important questions. As usual, though, the answers are not straightforward.

In the United States, one way of measuring growth in any sector of the economy is through the data collected by the US Bureau of Economic Analysis (BEA). Figure 1, which is based on the work of Matt Leichter,1 shows the growth in the US economy (as GDP) on the left scale and the contribution to GDP made by the legal sector as defined by the BEA (legal sector value added)2 on the right, for roughly the past four decades. Figures are presented in constant 2005 dollars, so as to correct for inflation.

Taking such a long view reveals a number of fascinating insights:

in the USA at least, the legal sector seems generally to be more susceptible to the impact of recessions than other sectors of the economy;

following a recession, the legal sector takes a lot longer to return to pre-recession peaks than the economy generally;

as the economy emerges from a recession, it appears that some of the demand in the legal sector is being taken up by a range of different services suppliers (e.g. in-house legal departments and other kinds of advisory service providers such as legal process outsourcing businesses, accounting firms and tax advisors)

the relative contribution that the legal sector contributes to GDP in the United States has been generally declining for roughly the past 25 years, probably through other kinds of legal service providers and in-house legal departments taking market share away from 'conventional' law firms; and

in real terms (constant 2005 dollars), the global financial crisis knocked the US legal sector back to levels that it had not seen since the mid 1990s.

Leichter's model suggests that recovery to pre-crisis levels is still some years away for the US legal sector. The downturn resulting from the savings and loan crisis, which was nowhere near as sharp nor deep as the contraction in 2008/9, took eight years to recover to pre-recession levels.

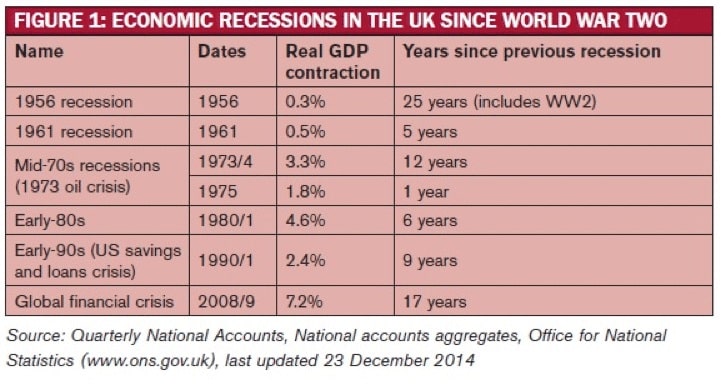

Figure 1: Economic recessions in the UK since WW2

In simple terms, this suggests that the US legal services market overall may be lucky to return to its 2008 levels in real terms before 2018 to 2020. Given that many premium firms sustained revenues and profitability generally through the recession and some have even grown them, recovery may take even longer for mid-tier and smaller firms.

To what degree might this hold true in the United Kingdom? The United States is the largest legal market in the world (accounting in recent years for roughly half the global legal spend), but most of that work is internal to the United States. The UK legal market is far more porous, with legal fees being earned in Britain on matters from a wide range of foreign jurisdictions too.

It is worth noting, for clarity, that the UK legal sector is defined as legal services produced within the United Kingdom by law firms. Hence, the German office of a UK law firm is excluded (it falls into the German legal market), but the London office of a US or German law firm, for instance, is included. Given that office financial data is not publicly reported, the economists had to use some carefully-formulated assumptions in order to derive this intelligence.

The Law Society of England & Wales estimates that net exports of legal services from the UK increased by 3.0 per cent in 2014 and would grow to 7.9 per cent in 2015, as real growth returns to both developed economies and emerging markets. Also, a lot of the restructuring work as a result of the euro crisis was done under English law, so the London offices of those premium law firms that participated in this (whether UK or US based) benefited from that.

It is therefore probably true that the legal sector did not contract as much in the United Kingdom as it did in the United States. According to the Law Society, we might expect the UK legal sector to reach its pre-crisis levels again (in real terms) in mid-2015. In a report it published in August 2014,3 3.8 per cent growth in real turnover was forecast for 2014, increasing to 4.9 per cent in 2015. This is significantly better than was previously anticipated.

Recovery in the UK has also not been generally limited exclusively to larger firms with international practices and smaller firms with well-focused and disciplined strategies. Improvements in the UK business sector and a robust housing market were noted to be the key drivers behind the Law Society's improved outlook, with increases in real household income adding further impetus next year, both directly and through further positive impact on the housing market. This has been to the benefit of smaller law firms too, although other pressures in the market continue to have a very strong negative impact on this segment of the sector.

Talking to bank managers and accountants who serve the legal sector, one hears widely divergent views on how well firms are translating increased revenues into greater profitability.

Costs are increasing, sometimes at more than the average rate of inflation, so increased revenues are not translating directly into increased profits. Salary inflation is a serious issue, especially at mid- to upper-level associate ranks following lower recruitment levels during the recession. Increased lateral hiring churn has also driven up partner compensation, in some cases very substantially.

In London, UK law firms have to contend with a stronger dollar and the greater muscle that has given US law firms in drawing away their top partner talent. The threat of the 'big four' global advisory firms capturing significant market share in upper mid-tier services remains on the horizon, at least for now, but few doubt that this will become a compelling competitive market pressure in the next few years.

On the other hand, efficiency initiatives such as more intelligent matter sourcing and legal project management, in-house lower-cost work resources, lean six sigma and better use of technology are also driving down transaction costs. Coupled with more sophisticated pricing techniques, this is having a buoyant impact on profitability.

These issues are not cyclical, however. While the recession may have accelerated their implementation, they are fundamentally a function of the systemic evolutionary pressures at play across the profession.

For some firms, the return to growth suggests an opportunity to increase scale. Consolidation has caused a number of firms that have not merged recently to move down the league tables. For some, a significant merger now would be a means of returning to the category in the league tables that they previously occupied, in terms of revenues at least. Whether such combinations create long-term value will depend on the degree to which other strategic synergies exist, leading to the firm securing more profitable work from better clients. Increasing scale simply for scale's sake has seldom proved a reliable value creator in any industry.

It is impossible to accurately predict how long the current period of growth will continue. Figure 2 shows the recessions that took place in the UK since the second world war (note that the dotcom crisis, which induced a recession in the USA in 2001, is missing as it induced a slowdown but not an actual recession in the UK).

If we exclude the period between the great depression and the 1956 recession as an anomaly because of the second world war falling into that period, an average of 8.3 years elapsed between the recessions.

On that basis, one might easily foresee another recession occurring within the next three to five years, being the period most usually adopted by law firms for a strategic planning horizon. How severe such a recession might be would depend on the nature of the trigger (a banking crisis in China or a deterioration in the Eurozone, for instance) and the knock-on effects that would have on economic systems still fragile from the impact of the global financial crisis.

Despite bolstering their business models between 2009 and 2012, many law firms' economic circumstances remain quite fragile. Continued profitability frequently remains dependent on a relatively small number of the firm's most productive partners and on a relatively small number of key clients. While one need not adopt an overly pessimistic view of the future, enhancing the firm's organisational resilience is today as important as having a clear view of the firm's preferred future and a strategy to achieve it.

Bolstering resilience and enhancing performance and market competitiveness generally are, of course, heavily intertwined. There are many 'levers' that law firm leaders can pull. Three of the most effective are probably as follows.

The pressures in the legal sector, most particularly on fees, have severely diluted the comfortable collegiality that used to exist in law firm partnerships. This is especially true for firms at the premium end of the market, whose talent is in high demand.

In such forms, resilience involves maintaining levels of profitability and compensation models that can retain the firm's top talent. This involves:

uncomfortable conversations with partners whose practices systemically underperform;

a compensation system that is competitive with other firms competing for the same talent;

lateral hiring away from other firms in cases where a solid business case exists as well as clear strategic and cultural alignment; and

working to actively grow the bench strength of the firm's talent.

It is disappointing that, in today's sophisticated market, the major league tables still define law firm success in terms of gross revenues/turnover and (average) profits per equity partner (PEP). While both provide important perspectives on performance, neither is really a good predictor of either resilience or growth potential.

The firms most likely to thrive are those that are best at knowing which parts of their business are driving their profits (not just revenues) and which are profit dilutive. This involves measuring profitability at a far more granular level:

by client;

by matter;

by service lines within practices;

by office; and

by fee-earner.

Careful thought and alignment with the firm's business model are vital to measuring the firm's sources of profitability and then using the information gleaned to inform strategy. For example, an office in a market with a depressed currency may be more important to firmwide profitability than its own revenues suggest, and allocating firmwide costs bluntly in dollars or pounds sterling to such an office may make it appear unprofitable.

Similarly, a firm's largest clients by revenue are frequently not its most profitable. Protective partners writing off time before it is properly recorded may mask unprofitable clients. Focusing too much on individual fee-earner performance promotes undesirable behaviour such as work hogging.

The more complete the picture of what drives the firm's performance, the easier it is to take the most appropriate management action.

Most sophisticated law firms have long segmented clients according to their importance to the firm and differentiate the levels that they provide to each per unit revenue. At its most basic level, this involves a key client programme. At a more sophisticated level, it may involve a more active approach to client industry sectors (focused on industry sectors in which the most important clients are aggregated) and other initiatives aimed at deepening relationships with those clients and broadening the firm's understanding of their businesses.

Law firm marketing pundits have said for years that all a firm's lawyers need to do in order to better understand how to meet the needs of their most important clients is to talk to and listen to those clients. This is one factor that has not changed at all since the global financial crisis, except to become even more important. In the UK, firms also have the option to look beyond pure legal services and to explore other kinds of services that can be easily bundled with them.

Strong growth has undoubtedly returned to the legal sector in terms of demand for legal services. Given the sharp decline that was experienced in 2009/10, it is unsurprising that the growth is proving quite pronounced. It remains to be seen, however, how much of that demand is satisfied by conventional law firms in years to come, versus being bled away to other kinds of legal service providers or in-house. It also remains to be seen which strategies that firms employ to respond to the renewed growth actually deliver sustained improvements in profitability.

As to the impact that another recession would have, as Warren Buffet said, "you never know who's swimming naked until the tide goes out". The pressures for short-term performance and returns to partners are inexorable, but this should not be at the expense of the firm's resilience against internal and external future knocks.

Credit to Author: Rob Millard is a partner and co-head of the strategy practice at the Møller PSF Group at Churchill College, within the University of Cambridge (www.mollerpsfgcambridge.com)

Original source material: https://www.solicitorsjournal.com/feature/business-strategy/strategic-resilience-protect-your-law-firm-future-recessions